Upcoming GBP/USD Analysis: Impact of UK GDP and Economic Indicators

As we approach the release of the latest UK GDP data, it is crucial to analyze the potential impact on the GBP/USD currency pair. Here’s a comprehensive overview of the current economic landscape and how it might influence trading decisions.

UK GDP Performance

The latest data from the Office for National Statistics (ONS) indicates that the UK economy has shown a modest growth trajectory. In August 2024, the monthly real GDP grew by 0.2%, following no growth in July 2024. This growth was driven by increases in all main sectors: services output rose by 0.1%, production output by 0.5%, and construction output by 0.4%[3].

On a quarterly basis, the UK GDP grew by 0.5% in the second quarter of 2024, although this was revised down from the initial estimate of 0.6%[1]. This growth, albeit modest, suggests that the UK economy is navigating through a period of stability, albeit with some downward revisions in previous quarters.

Sectoral Contributions

The services sector, which is the largest contributor to the UK's GDP, grew by 0.1% in August 2024 and by the same margin over the three months to August 2024 compared to the three months to May 2024. Production output, after a revised fall in July, rebounded with a 0.5% increase in August, while construction output also showed a 0.4% rise[3].

Economic Outlook and Inflation Concerns

The UK economy is still grappling with inflation concerns, despite recent labor figures exceeding expectations. Wages growth continues to elevate inflation worries, and the Bank of England's (BoE) upcoming Monetary Policy Report will be closely watched for hints on how the BoE plans to manage these pressures[2].

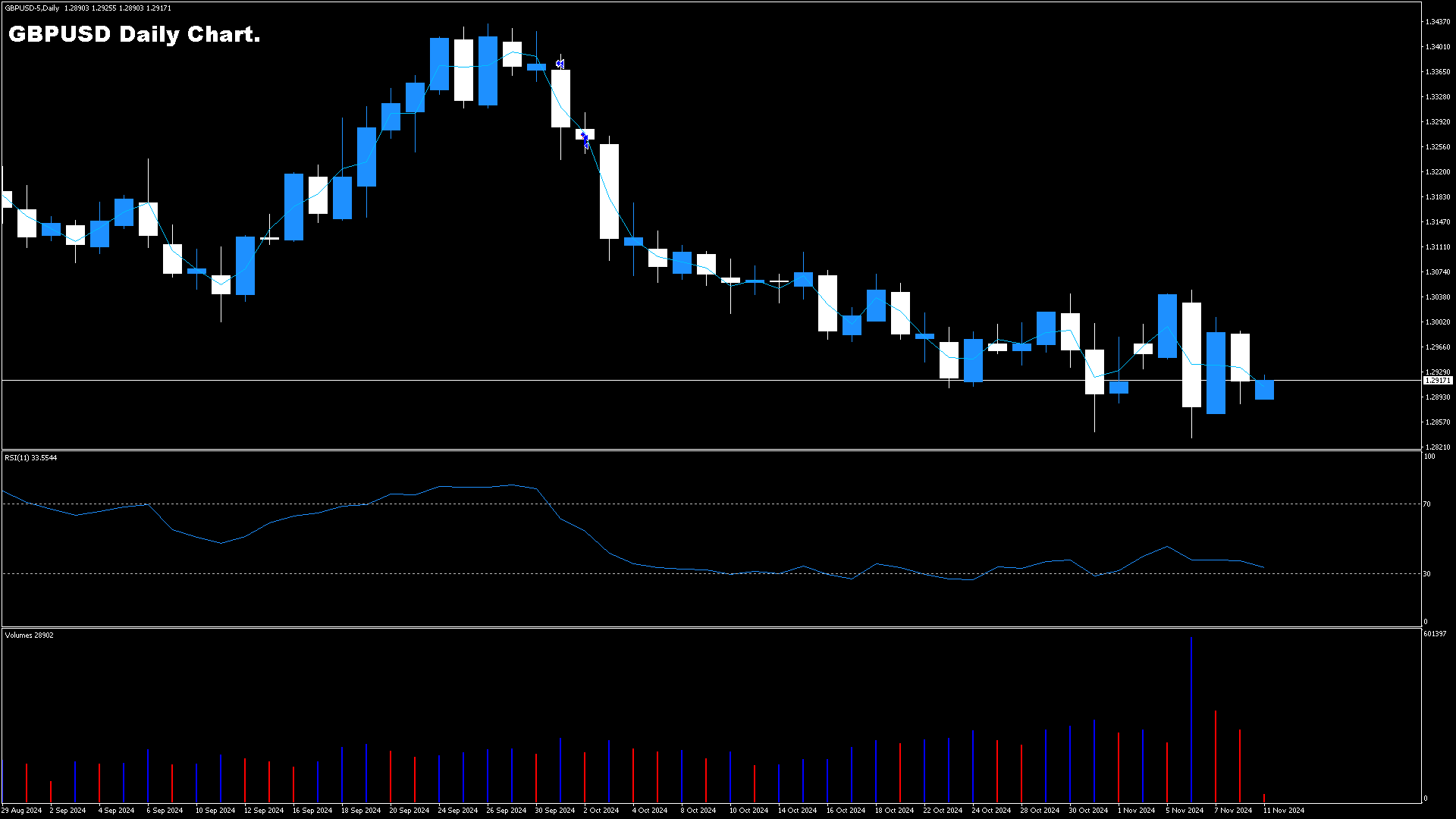

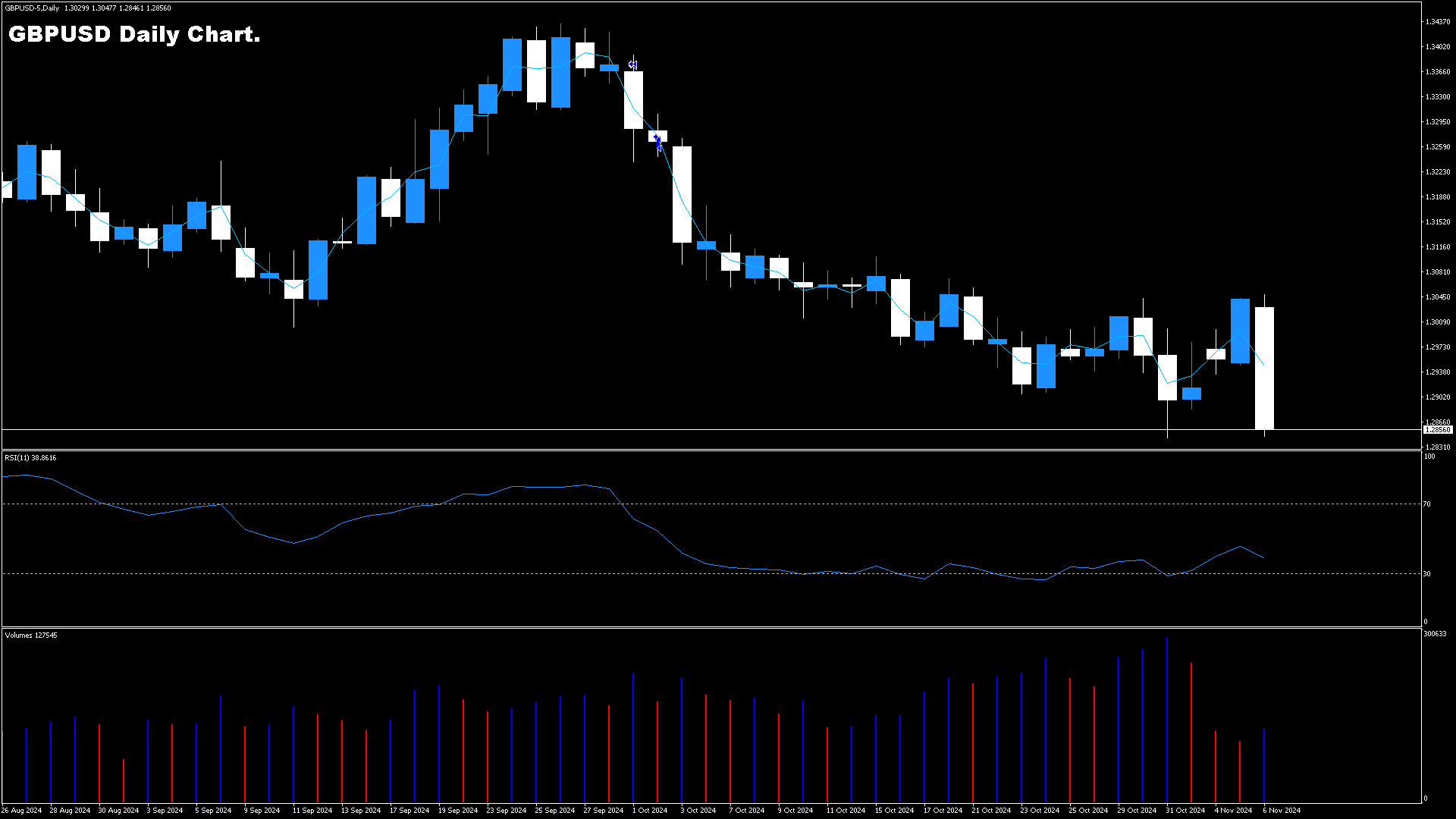

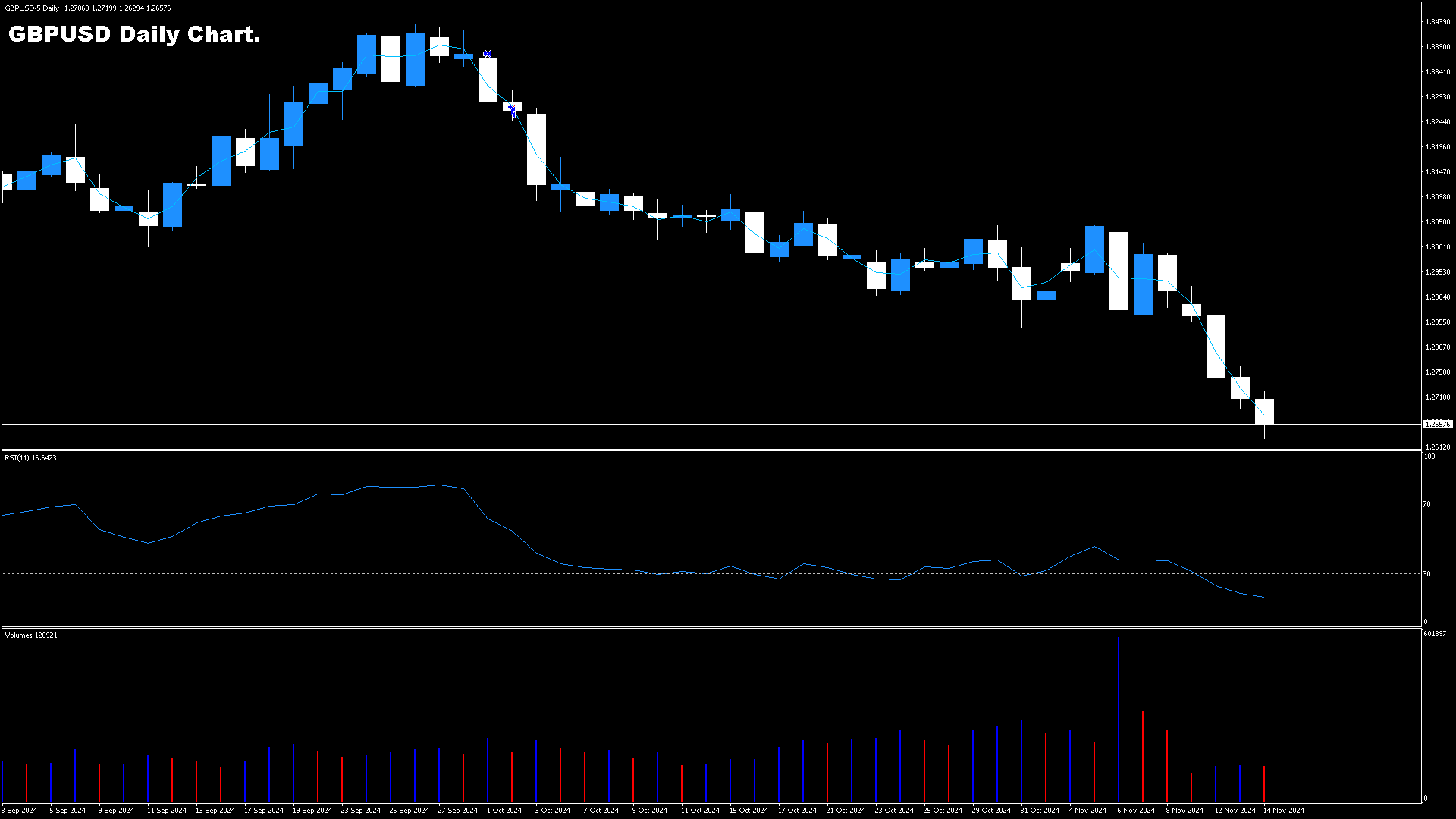

Impact on GBP/USD

The GBP/USD pair has been under significant pressure recently, with the pair breaking below key support levels and intensifying selling pressure. The daily chart shows the pair below the 200-day EMA (1.2868), which has turned into resistance, indicating a bearish trend[2].

However, positive GDP data could provide a temporary boost to the pound. If the upcoming GDP figures align with or exceed expectations, it could strengthen the pound against the US dollar, at least in the short term. This is particularly relevant given the current bearish momentum and the anticipation of economic and political events in 2024, including the UK general election and potential rate cuts by the BoE[2].

Technical and Fundamental Analysis

From a technical perspective, the GBP/USD pair needs to reclaim the 200-day EMA to signal a potential reversal of the bearish trend. Until then, the 50-day EMA (1.3014) remains well above the current price, reinforcing the bearish momentum[2].

Fundamentally, the pair is influenced by broader economic policies and global market shifts. The US Consumer Price Index (CPI) inflation figures, expected to show a slight increase, and the US retail sales data will also play a crucial role in determining the direction of the GBP/USD pair. Any signs of easing inflation in the US could lead to a more dovish stance by the Federal Reserve, potentially weakening the US dollar and supporting the pound[2][5].

Forecast and Predictions

Analysts have mixed views on the GBP/USD pair's future trajectory. Some forecasts suggest the pair could trade within a range of 1.313 to 1.378 by the end of 2024, driven by positive economic indicators and a relative weakening of the US dollar[4].

However, other predictions indicate a bearish trend, with the pair potentially declining to around 1.309 by the end of the year. The uncertainty is heightened by looming economic and political events, including the prospect of a recession and general elections in both the UK and the US[2][4].

Conclusion

As traders and investors await the upcoming UK GDP data, it is essential to consider both the technical and fundamental factors influencing the GBP/USD pair. Positive GDP figures could provide a short-term boost to the pound, but the overall trend remains bearish unless significant support levels are reclaimed.

Given the complex interplay of economic indicators, monetary policy decisions, and political events, staying informed and adaptable is crucial for making informed trading decisions in the highly volatile GBP/USD market.