Upcoming Canadian Employment Change: Key Insights and Market Implications

As the financial markets prepare for the release of Canada's September employment data, traders and investors are keenly watching the potential impact on the Canadian dollar (CAD) and the broader economic landscape. Here’s a detailed analysis of what to expect and how this data could influence your trading decisions.

Expected Job Growth and Unemployment Rate

The Canadian employment report, scheduled for release, is anticipated to show a modest increase in job growth. Market expectations were for an addition of 27,000 jobs, slightly higher than the 22.1 thousand jobs added in August. However, the actual figure came in significantly higher at 46.7 thousand jobs, exceeding expectations.

The unemployment rate is projected to tick up to 6.7% from 6.6% in August, but the latest data revealed a rate of 6.5%, which is better than anticipated.

Impact on the Canadian Dollar (CAD)

The release of the Canadian Employment Change data has significant implications for the CAD. A strong labor market, as indicated by the higher-than-expected job growth, is generally viewed as a positive sign for the Canadian economy. This can lead to increased investor confidence and demand for the CAD, potentially causing it to appreciate against other currencies.

However, the immediate market reaction to the September data saw the USD/CAD pair fall by 45 pips as the market re-evaluated the likelihood of a Bank of Canada (BoC) rate cut. This reaction underscores the dynamic nature of market responses to economic data.

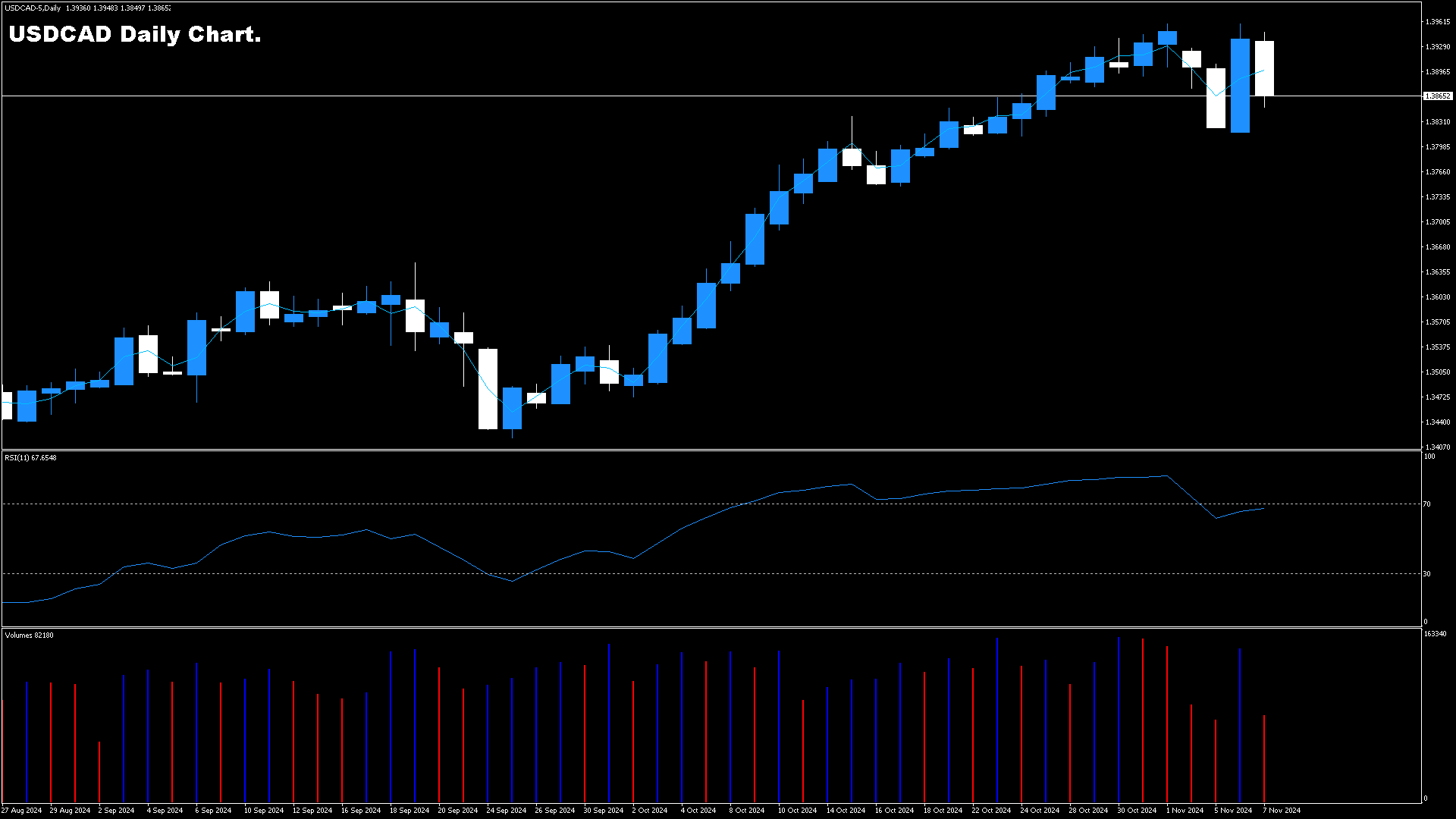

Technical Analysis for USD/CAD

In the lead-up to the employment report, the USD/CAD pair had been on a seven-day slide, with the Canadian dollar weakening to its lowest level against the US dollar since August 7. At the time of writing, USD/CAD was trading at around 1.3767, with key resistance levels at 1.3782 and 1.3822. Support levels are identified at 1.3735 and 1.3695.

Economic Context and Central Bank Policy

The Bank of Canada has been at the forefront of the recent rate-cutting cycle, having reduced rates by a quarter-point three times this year, bringing the cash rate down to 4.25%. Despite these cuts, the Canadian economy has been slow to respond, and the BoC is expected to continue monitoring and adjusting rates to keep them aligned with those in the US. The Federal Reserve’s expected rate cuts in November and December will also be closely watched by the BoC.

Detailed Breakdown of Employment Data

The September employment report provided several key insights into the Canadian labor market:

- Full-time Employment: Saw a significant increase of 112,000 jobs, the largest since May 2022, contrasting with a decline of 43.6 thousand in the previous month.

- Part-time Employment: Decreased by 65.3 thousand jobs, a reversal from the 65.7 thousand increase in the prior month.

- Participation Rate: Dropped to 64.9% from 65.1% in the previous month, which somewhat tempers the positive impact of the lower unemployment rate.

- Average Hourly Wages: Grew at a year-over-year rate of 4.5%, down from 4.9% in the previous month.

Trading Strategies and Preparation

To effectively trade the Canadian Employment Change, it is crucial to be well-prepared:

- Economic Calendar: Keep track of the release date and time of the employment data to plan trading activities in advance.

- Market Sentiment: Analyze market expectations and sentiment before the data release to anticipate potential price movements.

- Risk Management: Implement robust risk management strategies, including position sizing, to handle the volatility that often accompanies major economic releases.

Conclusion

The Canadian Employment Change data is a critical economic indicator that can significantly influence the value of the CAD and broader market dynamics. With the latest data exceeding expectations, traders should be prepared for potential shifts in market sentiment and central bank policy. By understanding the underlying economic factors and employing a well-thought-out trading strategy, investors can navigate the volatility and make informed decisions in response to this key economic event.