Upcoming Swiss Consumer Price Index (CPI) - Monthly Analysis and Implications

As we approach the release of the Swiss Consumer Price Index (CPI) for the month, market participants and economists are keenly watching the data for insights into the current state of inflation in Switzerland. Here’s a detailed analysis of what to expect and the potential implications for the Swiss franc (CHF) and broader economic policies.

Current Inflation Landscape

The latest available data indicates that the Swiss CPI has been relatively stable but slightly below expectations. In the previous month, the annual inflation rate stood at 0.8%, which is lower than the forecasted 1.1% and the previous month's 1.1%.

For the upcoming release, the monthly CPI is expected to be flat at 0.0%, compared to a -0.3% decline in the previous month. This stability suggests that inflationary pressures in Switzerland are currently under control, aligning with the Swiss National Bank's (SNB) target of keeping inflation below 2% over the medium term.

Factors Influencing CPI

Several factors have contributed to the recent inflation trends in Switzerland. Higher housing rents and costs associated with international holidays have been significant drivers of inflation, while decreases in prices of items like heating oil and certain food products have offset these increases.

Retail Sales and Economic Activity

Recent retail sales data have shown a surprising rebound, with a 2.7% year-over-year increase in July, significantly beating market estimates. This robust performance indicates strong consumer spending, which can influence CPI readings and overall economic health.

Monetary Policy Implications

The SNB closely monitors CPI data to make informed decisions on monetary policy. With the current inflation rate below the 2% target, the SNB may not feel immediate pressure to tighten monetary policy. However, any unexpected rise in CPI could prompt the central bank to consider raising interest rates to maintain price stability.

Exchange Rate Implications

The Swiss franc is highly sensitive to CPI data. Higher-than-expected inflation figures could lead to a strengthening of the CHF as market participants anticipate tighter monetary policy from the SNB. Conversely, lower-than-expected figures might result in a weakening of the CHF, as it could indicate a looser monetary policy stance.

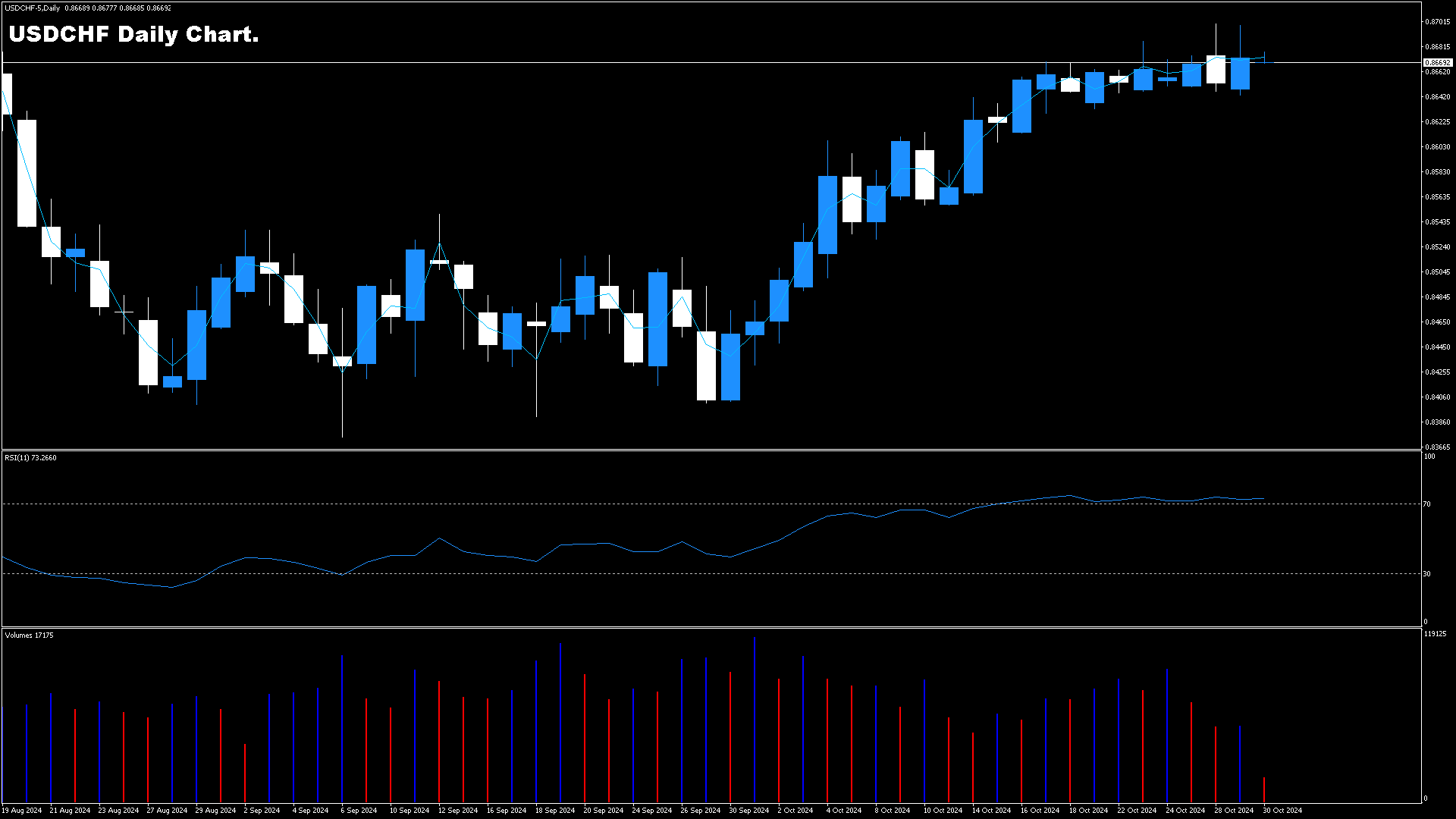

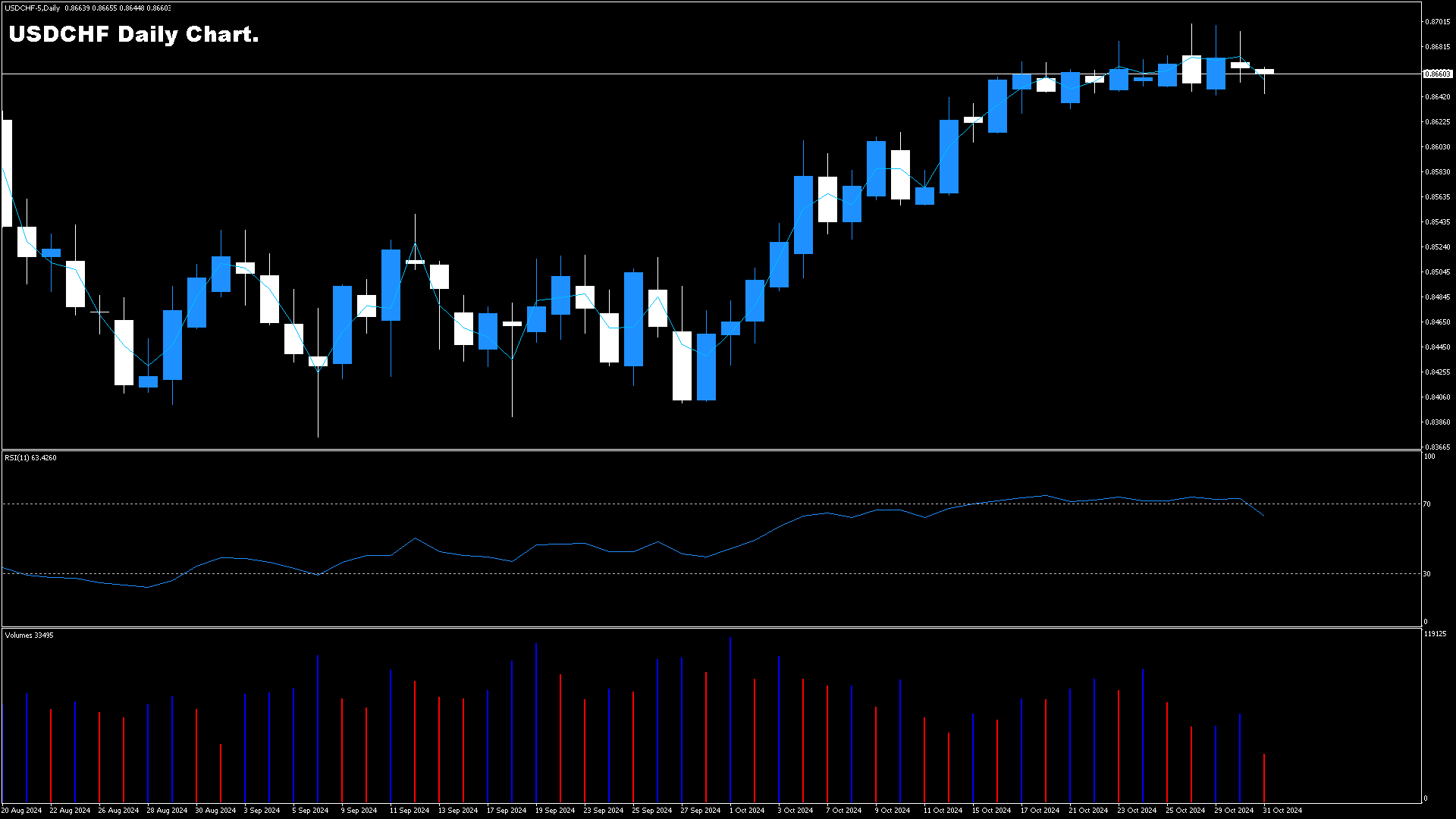

Technical Analysis for USD/CHF

From a technical perspective, the USD/CHF pair has been volatile, influenced by both Swiss and US economic data. Key resistance levels are at 0.8520 and 0.8541, while support levels are at 0.8491 and 0.8470. Any significant deviation in the CPI data could push the pair beyond these levels, depending on the market's reaction to the inflation figures.

Global Economic Context

The global economic landscape also plays a crucial role in shaping the Swiss economy and the value of the CHF. With other major economies like the Eurozone and the US releasing key economic indicators around the same time, the Swiss CPI data will be evaluated in the context of broader global trends. For instance, the Eurozone Flash CPI and US labor market data will also influence market sentiment and currency movements.

Conclusion

The upcoming Swiss CPI data will be a critical indicator of the country's inflationary pressures and will have significant implications for monetary policy and the value of the Swiss franc. Market participants should be prepared for potential volatility in the USD/CHF pair and other CHF crosses, depending on whether the actual CPI figures align with or deviate from market expectations.

As always, the SNB's response to the CPI data will be closely watched, as it will provide clues about future interest rate decisions and other monetary policy actions aimed at maintaining price stability in Switzerland.